Create professional development programs that help REALTORS® strengthen their businesses.

Create professional development programs that help REALTORS® strengthen their businesses.

Protect private property rights and promote the value of REALTORS®.

Protect private property rights and promote the value of REALTORS®.

Advance ethics enforcement programs that increase REALTOR® professionalism.

Advance ethics enforcement programs that increase REALTOR® professionalism.

Protect REALTORS® by providing legal guidance and education.

Protect REALTORS® by providing legal guidance and education. Stay current on industry issues with daily news from Illinois REALTORS®, network with other professionals, attend a seminar, and keep up with industry trends through events throughout the year.

Stay current on industry issues with daily news from Illinois REALTORS®, network with other professionals, attend a seminar, and keep up with industry trends through events throughout the year.

Understanding the U. S. Treasury Department rules for short sales can be challenging but the Department is aiming to make that process more streamlined and simplified. The Home Affordable Foreclosure Alternatives (HAFA) Program provides additional options to avoid costly foreclosures and offers incentives to borrowers, servicers and investors who utilize a short sale or deed-in-lieu (DIL) to avoid foreclosures.

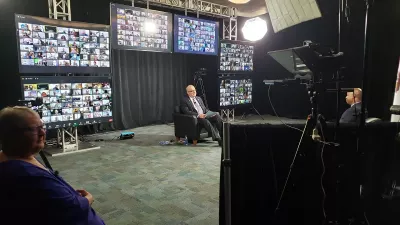

U.S. Treasury and Fannie Mae officials, IAR officers and staff host a statewide industry outreach meeting via video conference from IAR headquarters in Springfield.

IAR leaders met with representatives of the U. S. Treasury Department and Fannie Mae on May 3 at the IAR headquarters in Springfield to discuss and explore the state of short sales/HAFA in Illinois. Laurie Maggiano, Director of Policy for the Treasury’s Homeownership Preservation Office, and Judy Majors, Senior Program Manager for Fannie Mae, listened to leaders and REALTORS® from around the state via conference call regarding impediments for HAFA and short sale process in Illinois.

On May 9 representatives from five states including Florida, California, Arizona, Nevada and Illinois will meet with mortgage servicers and Treasury officials in Washington, D.C., to discuss issues with the short sale process, best practices with HAFA program and short sales and what improvements need to be made to streamline the processes. Sharon Gorrell, IAR Housing Policy Advisor and IAR President-elect REALTOR® Loretta Alonzo will represent IAR at this summit.

“We are working hard to develop positive stories with the HAFA program and we want to identify issues and solutions,” Maggiano told leaders at the meeting. “We are interested in hearing from REALTORS® about their experiences in the short sales both good and bad.”

REALTORS® are urged to submit their comments regarding their experiences with short sales online to IAR at [email protected] to be be shared with Treasury officials.

Maggiano explains once the borrower successfully completes the HAFA program it should help the borrower get back on their feet financially and be free of mortgage debt once the home is sold in short sale. Determining the true picture of financial hardship has been a challenge for some borrowers in gaining acceptance to the HAFA program, REALTORS® say.

REALTORS® reported some borrowers they have worked with are denied participation in the program even though financial hardship is evident—leaving them perplexed and helpless through lack of acceptance in the program and facing no further options but foreclosure on their home if the mortgage servicer does not accept a short sale option.

REALTORS® who are assisting homeowners in this process and have questions regarding borrower’s qualifications in HAFA should e-mail: [email protected] to get quick access to questions. By sending the borrower’s loan amount and details of the case, it is the job of contact servicers employed by the U. S. Treasury through this website to follow up to make sure rules are being followed by mortgage providers.

Further information regarding HAMP administration can be found at http://www.hampadmin.com. REALTORS® can download the Making Home Affordable Handbool (pdf), view a schedule of upcoming live webinars and loan reporting documents, learn more at the HAFA online learning center and gain access to useful tools including programs and service and borrower documentation. While Fannie Mae and Freddie Mac have their own user guides for short sale processes, they are pretty much following the HAFA guidelines, Maggiano indicates.

“Short sales are clearly better for mortgage service providers than foreclosure. Changing the servicer behavior is a slow process but they are coming around,” says Maggiano. “We are still working to streamline the process in terms of documentation. HAFA has a single document for the short sales process. We are front-loading the process to try to put borrowers with servicers to give them time to market the home at a pre-approved price. In the Treasury program they have to show bonafide hardship. The relationship with the subordinate lien holder is the most difficult part of the short sale.”

Adds Maggiano: “Individuals must meet rules of ownership including they must have lived in the home as their primary residence in the last 12 months; the home has to meet local conforming loan limits for most areas of Illinois that is $417,000 and the loan must have originated before 2009. The individual must demonstrate hardship, unable to make mortgage payments.”

Maggiano indicates REALTORS® have a vital role to play in the process. “Borrowers need help in understanding their options and they trust the REALTOR® who comes into their living room and gives them good advice and shares with them their options. It is clearly evident the borrower is intimidated by other servicers. REALTORS® need to reach out to borrowers to help them in understanding the HAFA program to inform them of their options.”

“We are only hearing the outliers, the bad stuff about short sales not working. We want to hear success stories as we know there are successes in the short sale process,” Maggiano says.

In order to do this—IAR has committed to helping provide more education and resources to REALTORS® through communications and education about HAFA programs. The Treasury Department is interested in delivering more education programs about HAFA rules. Plans are being made for a HAFA short sale presentation at the fall IAR convention, October 11-13, at the Pheasant Run in St. Charles.